ESG Investing: A Complete Guide for UK Investors and Businesses

ESG Investing: A Complete Guide for UK Investors and Businesses

Last updated: 24 June 2026 | Author: VerdaScope Editorial Team

ESG investing is the practice of incorporating environmental, social, and governance factors into investment analysis and portfolio decisions—alongside traditional financial metrics. For UK businesses, ESG investing matters whether you are allocating pension scheme assets, evaluating shareholder pressure, or deciding how your own sustainability performance affects access to capital. For individual investors, it shapes how ESG funds UK providers market products and what disclosures you should expect under evolving regulation.

This pillar page is the hub for Green Finance & Investment. It explains what is ESG investing, how it relates to sustainable investing, responsible investing, and socially responsible investment (SRI), and routes you to practical guides on impact investing, green finance, and green bonds. This is general information, not financial advice.

Direct Answer

ESG investing means assessing investments using environmental, social, and governance criteria—such as climate risk, labour practices, and board oversight—alongside financial return objectives. In UK markets, sustainable investing and responsible investing often overlap with ESG but may emphasise different outcomes: risk management, values alignment, or measurable impact. The Financial Conduct Authority’s (FCA) Sustainability Disclosure Requirements (SDR) regime, finalised in Policy Statement PS23/16 (November 2023), introduced an anti-greenwashing rule, investment labels, and disclosure rules for certain UK retail products. Investors and businesses should treat sustainability claims as regulated statements requiring evidence—not marketing shorthand.

Key Takeaways

- ESG investing integrates environmental, social, and governance factors into investment decisions; it is not a single product type or guaranteed “ethical” outcome.

- UK sustainable investing spans ESG integration, exclusions, thematic funds, stewardship, and impact investing—approaches differ in intent and measurement.

- The FCA’s SDR package aims to make sustainability references fair, clear, and not misleading for FCA-authorised firms.

- ESG investment criteria vary by fund, index, and rating provider; compare binding portfolio rules, not brochure adjectives.

- Businesses seeking capital should align ESG reporting with investor expectations and avoid overstating transition progress.

- For greenwashing risks in funds, see greenwashing in ESG investing.

- Next steps: compare impact investing vs ESG, explore green finance for businesses, and understand ESG fundamentals.

Topic Map: Green Finance & Investment Pillar

| Cluster | What you’ll learn | Go deeper |

|---|---|---|

| ESG investing | Definitions, approaches, UK regulation, fund evaluation | This page |

| Impact investing | Intentional, measurable social/environmental outcomes | Impact investing guide |

| Green finance | Loans, bonds, and public finance for sustainable projects | Green finance guide |

| Green bonds | Use-of-proceeds debt and UK issuance frameworks | Green bonds guide |

| ESG fundamentals | Corporate E, S, and G reporting context | What is ESG |

| Greenwashing in finance | FCA SDR, fund labels, due diligence | ESG greenwashing |

What Is ESG Investing?

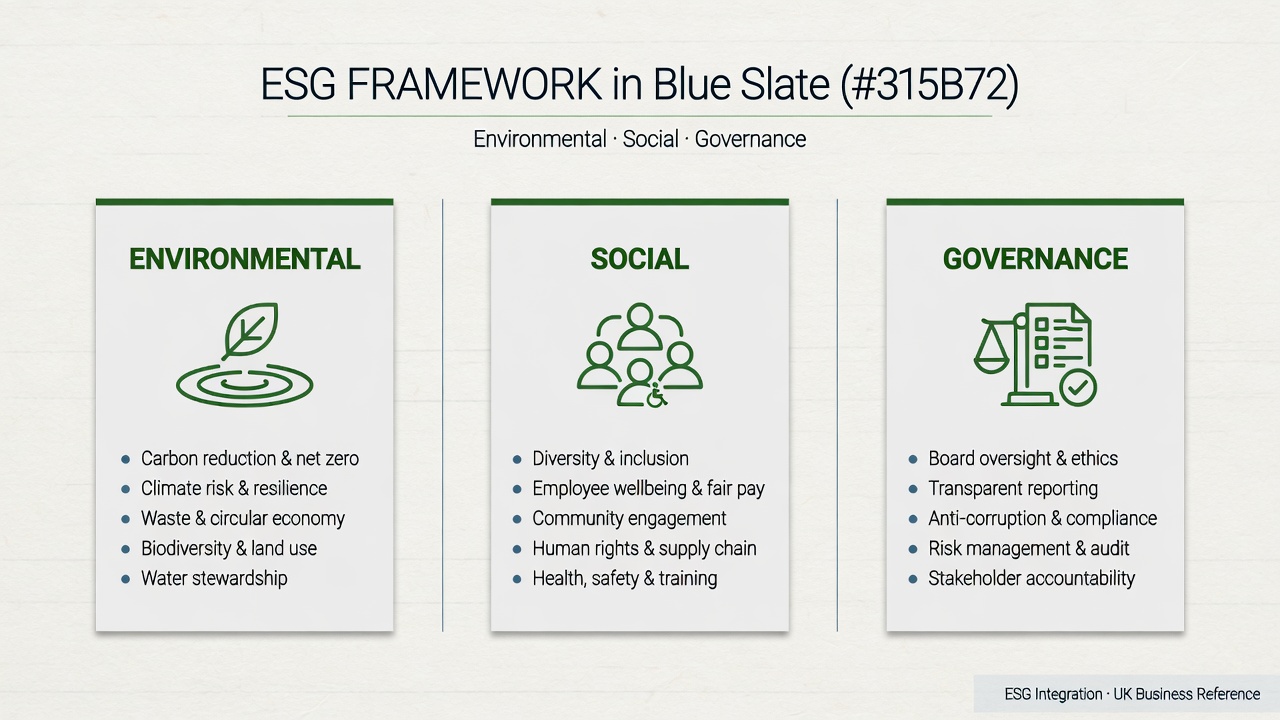

What is ESG investing? At its core, it is an investment approach that considers environmental, social, and governance factors when selecting, weighting, or engaging with assets. Environmental factors may include greenhouse gas emissions, energy use, pollution, and climate transition plans. Social factors may include workforce safety, diversity, human rights in supply chains, and community impact. Governance factors may include board independence, executive pay, audit quality, and anti-corruption controls.

ESG investing does not mean sacrificing returns by default. Many asset managers describe ESG as risk and opportunity analysis: climate regulation, litigation, reputational damage, or resource efficiency can affect long-term company value. Others pursue values alignment (excluding certain sectors) or thematic exposure (e.g. renewable energy). The label “ESG” alone does not tell you which approach applies—you must read fund documentation.

ESG investing vs sustainability vs responsible investment

| Term | Typical focus | Common UK usage |

|---|---|---|

| ESG investing | Structured E, S, G factor analysis in portfolios | Fund names, ratings, institutional mandates |

| Sustainable investing | Long-term economic and environmental sustainability | Broad marketing term; often overlaps with ESG |

| Responsible investing | Fiduciary duty, stewardship, risk management | Pension trustees, asset owner policies |

| Socially responsible investment (SRI) | Values-based screening (positive/negative) | Older term; still used in retail and charity contexts |

| Impact investing | Measurable positive outcomes alongside return | Social enterprises, outcomes contracts—see impact investing |

For corporate issuers, investor ESG questions usually trace back to what is ESG disclosure—emissions data, governance structures, and strategy credibility.

A Brief History: From SRI to Mainstream ESG

Socially responsible investment has roots in religious and ethical exclusions (e.g. avoiding tobacco or weapons) and activist shareholder campaigns. From the 2000s, responsible investing frameworks emphasised fiduciary duty: pension trustees should consider long-term risks, including environmental and social issues, where material to returns.

The ESG acronym gained traction after the 2004 UN Global Compact report Who Cares Wins, which argued that embedding environmental, social, and governance issues in capital markets could improve efficiency and sustainable development. Since then:

- Rating agencies and data vendors built ESG scores (methodologies differ significantly).

- Indices launched ESG-screened or low-carbon variants.

- Regulators moved from voluntary climate disclosure toward mandatory reporting (e.g. UK TCFD-aligned requirements for premium listed companies).

- Retail demand grew for ESG funds UK platforms list in ISAs and pensions.

The result is a large, heterogeneous market where “ESG” can mean anything from light-touch data integration to strict fossil-fuel exclusions. UK regulation is now catching up to marketing proliferation.

Main Approaches to ESG and Sustainable Investing

Understanding ESG investment criteria starts with recognising distinct portfolio strategies. A fund marketed as “sustainable” may use one or a combination of these:

1. ESG integration

The manager uses ESG data to inform risk/return analysis. Holdings may still include controversial sectors if deemed financially attractive and “materiality” does not warrant exclusion. Integration alone does not guarantee portfolio decarbonisation.

2. Negative screening (exclusions)

The fund excludes sectors or issuers (e.g. tobacco, controversial weapons, thermal coal). Exclusion lists and thresholds vary. Small exclusions relative to a benchmark may have limited portfolio effect.

3. Positive / best-in-class screening

The fund overweight companies with stronger relative ESG performance within a sector. This can still include oil and gas if selected issuers score better than peers.

4. Thematic investing

The fund targets a theme—clean energy, water, sustainable agriculture—with revenue or capex thresholds defining eligibility.

5. Stewardship and engagement

The manager votes at AGMs and engages with companies on ESG issues. Engagement can complement any strategy but should not be confused with automatic impact.

6. Impact investing

Investments target measurable social or environmental outcomes, often with explicit intent. See impact investing vs ESG for a detailed comparison.

| Approach | Primary objective | Typical evidence |

|---|---|---|

| ESG integration | Risk-adjusted returns | ESG ratings, research reports |

| Exclusions | Values alignment | Published exclusion list |

| Thematic | Exposure to sustainability theme | Revenue/capex thresholds |

| Stewardship | Influence issuer behaviour | Voting records, engagement reports |

| Impact | Measurable outcomes | Impact metrics, theory of change |

Why ESG Investing Matters for UK Businesses

Even if your organisation does not manage external funds, ESG investing trends affect you directly.

Access to capital

Lenders and investors increasingly review ESG strategy, climate risk, and disclosure quality. Private equity, bond investors, and banks may ask for scope 1, 2 and 3 emissions data, governance policies, and transition plans aligned with net zero pathways.

Cost of capital and loan pricing

Sustainable finance instruments—green loans, sustainability-linked loans (SLLs), and bonds—may offer pricing linked to sustainability performance targets. See green finance guide.

Reputation and greenwashing risk

Overstated sustainability claims in annual reports or investor presentations can attract regulatory scrutiny. The Competition and Markets Authority (CMA) Green Claims Code applies to corporate consumer-facing claims; investment-related communications by FCA-authorised firms fall under FCA rules. Misalignment between corporate claims and fund holdings feeds ESG greenwashing concerns.

Employees and pensions

UK employers selecting workplace pension defaults increasingly encounter sustainability-labelled funds. Trustees must balance member preferences, fiduciary duty, and regulatory disclosure—not marketing labels alone.

UK Regulatory Context: FCA SDR and HM Treasury Roadmap

UK sustainable investment regulation sits within a wider green finance policy framework. HM Treasury’s Greening Finance: A Roadmap to Sustainable Investing (October 2021) set out a phased plan to align financial flows with the UK’s net-zero commitment, including economy-wide Sustainability Disclosure Requirements (SDR) and consumer-focused investment labels developed by the FCA.

FCA Sustainability Disclosure Requirements (SDR)

The FCA finalised SDR rules in Policy Statement PS23/16 (November 2023). Key elements include:

| Element | Purpose |

|---|---|

| Anti-greenwashing rule | Sustainability references by FCA-authorised firms must be fair, clear, and not misleading |

| Investment labels | Four labels for qualifying UK authorised retail funds with defined criteria |

| Naming and marketing | Restrictions on sustainability-related terms where criteria are not met |

| Disclosures | Consumer-facing and detailed product-level sustainability disclosures |

| Distributor obligations | Requirements for firms distributing labelled products |

Investment labels (summary)

As described in PS23/16, labels include:

| Label | Plain-language intent |

|---|---|

| Sustainability Focus | Assets invested mainly in sustainable assets per defined criteria |

| Sustainability Improvers | Assets with potential to improve sustainability over time |

| Sustainability Impact | Assets with measurable positive environmental/social impact |

| Sustainability Mixed Goals | Mix of sustainability objectives under defined criteria |

Labels require firms to meet specific criteria before use and to notify the FCA. They are not a guarantee of superior returns or zero controversy holdings—read the consumer disclosure document.

Implementation timing

PS23/16 sets phased implementation dates (including the anti-greenwashing rule, label availability, and naming/marketing requirements). Verify current effective dates and any subsequent FCA updates on fca.org.uk before relying on timelines—rules may be amended after publication.

EU SFDR (cross-border context)

UK readers holding EU-domiciled funds may encounter SFDR Article 6, 8, or 9 categories. These are not equivalent to UK SDR labels. Do not assume Article 8 “promotes environmental characteristics” equals a UK Sustainability Focus label. See greenwashing in ESG investing for parallel EU issues.

Corporate disclosure linkage

Investors rely on issuer disclosures. UK large companies face climate-related reporting expectations; sustainability reporting is evolving toward ISSB-aligned UK standards. Businesses should ensure sustainability reporting consistency across annual reports, TCFD disclosures, and investor presentations.

ESG Funds UK: Product Landscape

ESG funds UK investors can access include:

- Active mutual funds and OEICs with ESG mandates

- Passive index trackers tracking ESG-screened or climate indices

- Exchange-traded funds (ETFs) with ESG or thematic strategies

- Multi-asset sustainable funds blending equities, bonds, and other assets

- Workplace pension defaults with responsible investment policies

Evaluating funds: a practical checklist

Educational framework only—not investment advice.

- Check for an FCA sustainability label (if UK authorised retail fund).

- Read the consumer disclosure and full prospectus—investment constraints must be binding.

- Review top holdings against stated strategy (exclusions, themes, impact goals).

- Compare naming and marketing to regulatory filings—misalignment is a red flag.

- Understand ESG data sources and whether scores drive selection or are informational only.

- Assess fees relative to non-ESG peers—“green” branding is not automatic justification for higher charges.

- Consider stewardship reporting if engagement is central to the strategy.

For a deeper due-diligence framework, see how to check ESG investments.

ESG Investment Criteria: What Investors Actually Measure

ESG investment criteria differ by manager, but common factor categories include:

Environmental

- Greenhouse gas emissions (absolute and intensity)

- Energy consumption and renewable share

- Water use and pollution incidents

- Waste and circular economy practices

- Biodiversity and land use (growing focus)

- Climate transition plans and capex alignment

Social

- Health and safety performance

- Workforce diversity and pay equity

- Labour standards in supply chains

- Product safety and data privacy

- Community relations and human rights

Governance

- Board independence and diversity

- Executive remuneration alignment

- Audit quality and internal controls

- Anti-bribery and whistleblowing policies

- Shareholder rights and related-party transactions

Materiality matters

Not every criterion applies to every sector. A software company and a mining company face different material ESG issues. Credible materiality assessment on the corporate side helps investors focus on what affects value and impact.

Ratings caution

Third-party ESG ratings can diverge for the same company. Treat ratings as one input—understand methodology, coverage, and timeliness. Do not equate a high rating with regulatory compliance or net-zero alignment.

ESG Investing for Different UK Stakeholders

Individual retail investors

- Use FCA-regulated platforms and read Key Investor Information Documents.

- Treat “sustainable,” “responsible,” and “ESG” as terms requiring definition in disclosures.

- Distinguish personal values from risk preferences—exclusion funds may differ from broad ESG integration funds.

- Seek regulated financial advice for personal circumstances if needed.

Pension trustees and employers

- Document investment beliefs on ESG and climate risk.

- Request evidence behind sustainability claims in default funds.

- Align member communications with fund prospectuses—avoid oversimplification.

- Consider stewardship policies and voting records where relevant to fiduciary duty.

Corporate finance and CFO teams

- Prepare investor-grade ESG data aligned with ESG reporting.

- Understand how your disclosure affects index inclusion and fund eligibility.

- If issuing labelled debt, follow recognised frameworks—see green bonds guide.

- Avoid claiming “ESG leader” status without benchmarked evidence.

SMEs

- Larger customers and lenders may request ESG questionnaires even without mandatory reporting.

- Start with material topics: energy, safety, governance basics, and supply chain policies.

- Green finance options may exist for eligible projects—see green finance.

Stewardship, Voting, and Active Ownership

Responsible investing increasingly emphasises stewardship—using shareholder rights to influence company behaviour on ESG issues. UK asset managers may publish:

- Voting policies on climate, remuneration, and board composition

- Proxy voting records showing how votes were cast

- Engagement case studies describing dialogues with issuers

Stewardship can support transition planning and governance improvements, but marketing should not imply that engagement alone delivers portfolio decarbonisation. A manager can vote for climate resolutions while still holding high-emission issuers awaiting transition.

Questions for stewardship claims

| Question | Why it matters |

|---|---|

| Are voting policies binding and public? | Distinguishes commitment from aspirational copy |

| Are votes disclosed at issuer level? | Enables verification |

| Are engagement goals linked to metrics? | Process alone is not outcome |

| Does stewardship cover fixed income holdings? | Bondholder engagement differs from equity voting |

UK pension schemes reviewing default funds should include stewardship quality alongside labels and fees—especially where members expect climate alignment.

UK Pension and Fiduciary Context (High Level)

Workplace pensions are a major channel for ESG funds UK retail exposure. Trustees operate under fiduciary duties defined in trust law and regulatory guidance. Key practical points:

- Investment beliefs documents increasingly reference climate risk and responsible investment.

- Statement of investment principles may describe ESG integration or exclusions.

- Member communications must not oversimplify fund characteristics—especially where sustainability language appears in member booklets but not in binding fund rules.

Employers selecting providers should ask:

- Does the default fund use an FCA sustainability label?

- What consumer disclosure accompanies the label?

- How do top holdings map to member-facing sustainability summaries?

This is governance due diligence for employers—not a recommendation to choose any particular fund.

Building an ESG-Aware Investment Policy (Businesses and Trustees)

Framework for organisations—not personal investment advice.

Step 1: Document objectives

Clarify whether the priority is risk management, values alignment, thematic exposure, or measurable impact. Objectives drive strategy selection.

Step 2: Define constraints

Liquidity needs, home bias, concentration limits, and exclusion policies (if any) should be explicit.

Step 3: Select strategy types

Map objectives to integration, exclusions, thematic, or impact sleeves—see impact investing where outcomes are primary.

Step 4: Set evidence standards

Require binding investment policy statements, reporting cadence, and—where relevant—assurance of ESG data used in decisions.

Step 5: Monitor and review

Review performance, risk, and sustainability reporting annually. Regulatory labels and fund names change; re-verify disclosures after rebrands.

Step 6: Align corporate issuer narrative

If your business also raises capital, ensure ESG reporting matches the story investors see in funds holding your securities.

Performance, Risk, and Common Misconceptions

Does ESG investing underperform?

Academic and industry studies reach mixed conclusions depending on period, methodology, and strategy type. ESG integration and exclusions can shift sector weights (e.g. technology vs energy), affecting relative performance in specific market cycles. Past performance does not predict future results. Sustainability labels do not eliminate market, credit, liquidity, or concentration risk.

Misconception: “ESG” means fossil-free

Many ESG funds integrate data without excluding fossil fuels. Always verify binding exclusions.

Misconception: Stewardship equals divestment

Engagement does not automatically change portfolio emissions. Managers may hold high-carbon issuers while engaging on transition plans.

Misconception: Impact labels guarantee measurable change

Impact requires defined metrics and baselines. UK SDR’s Sustainability Impact label has specific criteria—still read limitations in disclosures.

Misconception: ESG is only for large listed companies

Private markets, real assets, and social enterprises participate in sustainable investing and impact investing with different disclosure norms. Due diligence standards should adapt accordingly.

Compliant vs Risky Approaches (Funds and Issuers)

| Risky pattern | More defensible approach |

|---|---|

| “100% sustainable portfolio” (undefined) | FCA label + consumer disclosure explaining objective and asset tests |

| “ESG leaders fund” without selection criteria | Published exclusion/selection rules and rebalance policy |

| “Impact fund” without metrics | Defined impact indicators, measurement approach, and limitations |

| Corporate “net zero” claim without scope 3 or capex detail | Aligned net zero strategy with transparent boundaries |

| Green bond marketing without use-of-proceeds reporting | ICMA Green Bond Principles framework and allocation reports |

Common Mistakes

- Choosing funds by name alone—“ESG,” “Climate,” or “Sustainable” in a title does not prove strategy.

- Ignoring SFDR/SDR jurisdiction—UK and EU rules differ; cross-border products need dual reading.

- Equating ESG scores with ethics—ratings measure disclosed data and provider methodology, not moral consensus.

- Businesses reporting inconsistent ESG data to investors vs customers—creates credibility and regulatory risk.

- Trusting impact marketing without baselines—outcome claims need measurement design.

- Assuming regulation eliminates greenwashing—SDR raises standards; due diligence remains essential.

Frequently Asked Questions

What is ESG investing?

ESG investing incorporates environmental, social, and governance factors into investment analysis and portfolio decisions alongside financial objectives. Approaches range from ESG integration and exclusions to thematic and impact strategies.

What is sustainable investing?

Sustainable investing is a broad term for investment approaches that consider long-term environmental and social sustainability. It often overlaps with ESG, responsible investment, and impact investing—but specific strategies vary by product.

What is responsible investing?

Responsible investing typically emphasises fiduciary duty, long-term risk management, and stewardship. Pension trustees and institutional asset owners commonly use this language in investment policy statements.

What is socially responsible investment (SRI)?

Socially responsible investment traditionally refers to values-based screening—excluding certain sectors or seeking positive social outcomes. It predates modern “ESG” marketing but remains in use, especially in charity and faith-based portfolios.

What are ESG funds UK investors offered?

UK investors can access ESG-labelled mutual funds, ETFs, multi-asset products, and pension defaults through regulated platforms. Product quality and strategy differ—read FCA labels and disclosures where applicable.

What are typical ESG investment criteria?

Common criteria include emissions, energy use, labour practices, health and safety, board governance, and business ethics. Material criteria vary by sector and fund mandate.

How does FCA SDR affect ESG investing?

SDR introduces an anti-greenwashing rule, optional investment labels with criteria, naming/marketing restrictions, and disclosures for certain UK retail funds. It aims to improve trust in sustainability references.

Is ESG investing the same as impact investing?

No. ESG investing often focuses on risk, integration, or relative performance within mainstream markets. Impact investing targets measurable positive outcomes with explicit intent. See impact investing vs ESG.

Can businesses benefit from ESG investing trends without issuing shares?

Yes. Strong ESG performance can influence bank lending, supply chain selection, and private equity interest. Green finance instruments also support eligible projects—see green finance guide.

Is this financial advice?

No. This guide provides general educational information. Investment decisions involve risk. Seek advice from an FCA-authorised adviser for personal recommendations.

Sources and Update Log

| Date | Update |

|---|---|

| 24 June 2026 | Initial publication: ESG investing pillar hub for UK readers |

Authoritative sources

- Financial Conduct Authority, Policy Statement PS23/16: Sustainability Disclosure Requirements (SDR) and investment labels, November 2023 — fca.org.uk

- HM Treasury, Greening Finance: A Roadmap to Sustainable Investing, October 2021 — gov.uk

- Competition and Markets Authority, Green Claims Code — gov.uk

Investment values can fall as well as rise. Verify current FCA rules and product disclosures before making decisions.

Next Steps

- Impact strategies → Impact investing guide

- Business funding → Green finance guide

- Debt instruments → Green bonds guide

- Fund greenwashing risks → Greenwashing in ESG investing

- Corporate ESG basics → What is ESG

- Reporting for investors → ESG reporting