Scope 1, 2 and 3 Emissions Explained: A Business Guide

Scope 1, 2 and 3 Emissions Explained: A Business Guide

Last updated: 24 June 2026 | Author: VerdaScope Editorial Team

Understanding scope 1 2 3 emissions is essential for credible carbon emissions reporting in the UK. These GHG emissions categories—defined by the Greenhouse Gas Protocol—form the basis of SECR disclosures, TCFD metrics, UK SRS S2 climate reporting, and customer supply chain questionnaires. This guide explains what each scope covers, what is scope 3 emissions, and how to approach emissions measurement practically.

Direct Answer

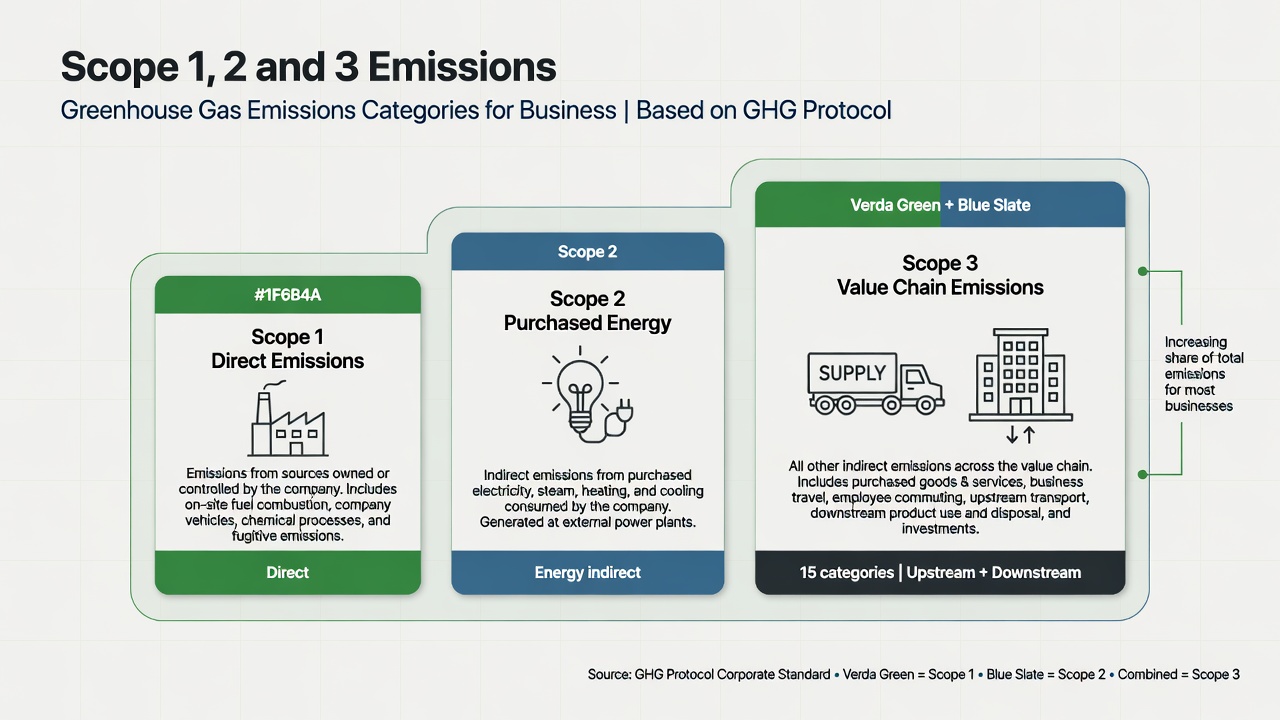

Scope 1 emissions are direct greenhouse gas emissions from sources owned or controlled by the company (e.g. gas boilers, company vehicles). Scope 2 emissions are indirect emissions from purchased electricity, heat, or steam. Scope 3 emissions are all other indirect emissions in the value chain (e.g. purchased goods, business travel, waste, product use). Together, scope 1, 2 and 3 emissions provide a full carbon emissions reporting picture when material categories are included.

Key Takeaways

- Scope 1 = direct emissions; Scope 2 = purchased energy; Scope 3 = value chain (15 categories).

- UK SECR requires Scope 1 and 2 for qualifying companies—not Scope 3.

- TCFD and UK SRS S2 expect Scope 3 disclosure when material.

- Scope 3 often represents the largest share for many businesses—especially in supply chains.

- Use GHG Protocol Corporate Standard and Scope 3 Standard for methodology.

- Start with Scope 1+2, then prioritise material Scope 3 categories incrementally.

Definition Table: Scope 1 vs Scope 2 vs Scope 3

| Scope | Definition | Who controls source? | Examples |

|---|---|---|---|

| Scope 1 | Direct GHG emissions | Company owns/controls | Gas heating, diesel fleet, on-site generators, refrigerant leaks, industrial processes |

| Scope 2 | Indirect from purchased energy | Company buys energy | Electricity, district heating, steam |

| Scope 3 | Other indirect value chain emissions | Third parties, but linked to company activities | Purchased goods, logistics, commuting, business travel, waste, product use, investments |

Scope 1 Emissions: Direct Emissions

What counts as Scope 1

- Combustion of fuels in boilers, furnaces, kilns

- Fuel in company-owned or controlled vehicles

- Fugitive emissions (refrigerants, SF₆, methane leaks)

- On-site manufacturing process emissions

- Emissions from company-owned generators

How to measure Scope 1

- Identify emission sources within organisational boundary

- Collect activity data (litres fuel, m³ gas, kg refrigerant)

- Apply emission factors (UK Government GHG Conversion Factors or IPCC)

- Sum tCO₂e (tonnes carbon dioxide equivalent)

UK context

SECR requires reporting Scope 1 emissions for in-scope companies. Use consistent DEFRA/DESNZ conversion factors updated annually.

Scope 2 Emissions: Purchased Energy

Location-based vs market-based

| Method | Definition | When to use |

|---|---|---|

| Location-based | Grid average emission factor for region | SECR minimum; default under GHG Protocol |

| Market-based | Reflects contractual instruments (REGOs, PPAs, RECs) | Voluntary reporting; shows renewable procurement |

SECR emphasises location-based Scope 2. Market-based may be reported additionally.

How to measure Scope 2

- Collect electricity and purchased heat consumption (kWh)

- Apply grid emission factor (location-based)

- For market-based, apply supplier-specific or residual mix factors where available

Scope 3 Emissions: Value Chain

What is scope 3 emissions?

Scope 3 emissions are indirect greenhouse gas emissions that occur in your upstream and downstream value chain—not from assets you own, but from activities your business depends on. For many organisations, scope 3 emissions represent 70–90%+ of total footprint.

Why Scope 3 matters for UK reporting

While SECR does not mandate Scope 3, stakeholders increasingly expect it:

- UK SRS S2 — disclose when material

- SBTi — typically required for validated targets

- Customer questionnaires — especially categories 1, 4, 6, 7

- CDP — supply chain modules score Scope 3 completeness

- Public sector procurement — PPN 06/21 carbon reduction plans reference value chain emissions

Treating Scope 1+2 as a “complete carbon footprint” when Scope 3 is material creates greenwashing exposure.

The 15 Scope 3 categories (GHG Protocol)

Upstream

- Purchased goods and services

- Capital goods

- Fuel- and energy-related activities (not in Scope 1 or 2)

- Upstream transportation and distribution

- Waste generated in operations

- Business travel

- Employee commuting

- Upstream leased assets

Downstream 9. Downstream transportation and distribution 10. Processing of sold products 11. Use of sold products 12. End-of-life treatment of sold products 13. Downstream leased assets 14. Franchises 15. Investments

Prioritisation approach

You do not need all 15 categories in year one:

- Screen all categories qualitatively or with spend-based estimates

- Identify largest/most material categories

- Quantify material categories with improving data quality over time

- Disclose methodology and exclusions transparently

Measurement methods

| Method | Accuracy | Effort |

|---|---|---|

| Spend-based | Low–medium | Low |

| Average-data | Medium | Medium |

| Supplier-specific | High | High |

| Hybrid | Medium–high | Medium |

Supply chain detail: sustainable supply chain management

Organisational and Operational Boundaries

Organisational boundary

Defines which entities are included—typically aligned with financial consolidation (equity share or control approach per GHG Protocol).

Operational boundary

Defines which emission sources are included per scope. Document exclusions clearly.

Consistency with SECR boundary is essential for UK reporters.

Reporting Requirements: SECR, TCFD, UK SRS

| Framework | Scope 1 | Scope 2 | Scope 3 |

|---|---|---|---|

| SECR | Required | Required (location-based) | Not required |

| TCFD | Required | Required | Encouraged when appropriate |

| UK SRS S2 | Required | Required | Required when material |

| CDP | Required | Required | Increasingly expected |

| SBTi | Part of inventory | Part of inventory | Usually required for target validation |

See SECR reporting guide, TCFD reporting guide, UK SRS.

Practical Measurement Workflow

Phase 1: Scope 1 and 2 (months 1–3)

- Map sites and energy sources

- Collect 12 months utility and fuel data

- Apply government conversion factors

- Calculate intensity metrics

- Include in SECR if in scope

Phase 2: Scope 3 screening (months 3–6)

- List all 15 categories

- Estimate each using spend-based or proxy data

- Rank by magnitude and influence

- Select top 3–5 categories for improvement focus

Phase 3: Scope 3 refinement (months 6–18)

- Engage suppliers for category 1 data

- Improve business travel and commuting data from expense/HR systems

- Model product use emissions if relevant (category 11)

- Document uncertainty and improvement plan

Link to carbon footprint guide and net zero guide.

Worked Calculation Examples

Example 1: Scope 1 — Company diesel fleet

| Input | Value |

|---|---|

| Annual diesel consumption | 45,000 litres |

| Emission factor (DEFRA 2025) | ~2.51 kg CO₂e per litre |

| Calculation | 45,000 × 2.51 ÷ 1,000 |

| Scope 1 result | ~113 tCO₂e |

Example 2: Scope 2 — Purchased electricity (location-based)

| Input | Value |

|---|---|

| Annual electricity | 1,200,000 kWh |

| UK grid factor (location-based) | ~0.207 kg CO₂e per kWh (use current DESNZ factor) |

| Calculation | 1,200,000 × 0.207 ÷ 1,000 |

| Scope 2 result | ~248 tCO₂e |

Use emission factors published for your reporting year on gov.uk.

Example 3: Scope 3 Category 6 — Business travel (spend-based screening)

| Input | Value |

|---|---|

| Annual air travel spend | £320,000 |

| EEIO emission factor (spend-based) | Category-specific factor from DEFRA or EPA EEIO |

| Output | Screening estimate for prioritisation—refine with flight-level data where material |

Spend-based methods are acceptable for screening; improve to activity-based data for material categories before setting reduction targets.

Biogenic Emissions and Renewable Energy

Biogenic carbon

Biomass combustion may produce biogenic CO₂ tracked separately from fossil Scope 1 in some frameworks. SECR and GHG Protocol have specific rules—document treatment clearly.

Renewable electricity

- Location-based Scope 2 uses grid average factor regardless of tariff

- Market-based Scope 2 reflects REGOs, PPAs, and supplier-specific factors

- Report both where useful for stakeholders; SECR requires location-based minimum

UK Business Examples

Office-based services company

- Scope 1: Minimal gas heating, company cars

- Scope 2: Electricity for offices

- Scope 3 (material): Business travel, employee commuting, purchased IT services

Manufacturing company

- Scope 1: Gas, on-site fuel, process emissions, fleet

- Scope 2: Electricity for plant

- Scope 3 (material): Purchased raw materials, upstream logistics, waste, product use

Retailer

- Scope 1: Refrigerant leaks (significant), delivery fleet

- Scope 2: Store electricity

- Scope 3 (material): Purchased goods, downstream logistics, product end-of-life

Scope 3 Category Detail: Where to Start

Category 1: Purchased goods and services

Usually the largest Scope 3 category for manufacturers, retailers, and services firms buying significant materials. Start with:

- Spend-based estimate using EEIO factors

- Focus on top 20 suppliers by spend

- Request supplier-specific data for critical items

Links to sustainable supply chain management.

Category 6: Business travel

Common priority for professional services. Data sources:

- Travel management company reports

- Expense system flight and rail bookings

- CO₂e from DEFRA factors per km or spend

Category 7: Employee commuting

Survey employees periodically; apply average distance and mode factors. Remote working may reduce commuting but increase home energy (often excluded from Scope 3 unless material).

Category 11: Use of sold products

Material for product manufacturers (energy-using products). Requires use-phase assumptions—document clearly to avoid overstating precision.

Carbon Emissions Reporting Standards Cross-Reference

| Standard / framework | Scopes required |

|---|---|

| GHG Protocol Corporate Standard | 1, 2; 3 voluntary but recommended |

| SECR (UK) | 1, 2 |

| TCFD | 1, 2; 3 when appropriate |

| UK SRS S2 | 1, 2, 3 when material |

| SBTi | 1, 2, 3 (most targets) |

| ISO 14064-1 | 1, 2, 3 organisational inventories |

Maintain one master inventory mapped to each framework’s presentation requirements.

Common Mistakes and Greenwashing Risks

| Mistake | Risk |

|---|---|

| Reporting Scope 1+2 only as “full footprint” | Misleading if Scope 3 is material |

| Excluding refrigerants | Under-reported Scope 1 |

| Wrong organisational boundary | Invalid comparisons |

| Outdated emission factors | Inaccurate inventory |

| Scope 3 claimed without methodology | Low credibility with investors |

| Double counting across scopes | Inflated or inconsistent totals |

Frequently Asked Questions

What are scope 1, 2 and 3 emissions?

The three categories of greenhouse gas emissions in the GHG Protocol: direct (1), purchased energy (2), and value chain (3).

What is scope 3 emissions?

Indirect emissions in the upstream and downstream value chain—such as suppliers, transport, travel, and product use—not from owned sources.

Which scope is usually largest?

Often Scope 3, especially purchased goods and services for manufacturers and retailers.

Does SECR require scope 3?

No. SECR requires Scope 1 and 2 and UK energy use. Scope 3 is voluntary under SECR but may be required by other frameworks.

How do I calculate scope 1 and 2 emissions?

Collect activity data (fuel, kWh), multiply by official emission factors, sum tCO₂e. UK Government conversion factors are standard for SECR.

What emission factors should UK companies use?

DESNZ/DEFRA GHG conversion factors for company reporting—updated annually on gov.uk.

When must scope 3 be reported?

Under UK SRS S2 when material; TCFD encourages when appropriate; SBTi typically requires for science-based targets.

What is the greenhouse gas protocol?

The most widely used global standard for corporate GHG accounting—Corporate Standard (Scope 1+2) and Scope 3 Standard.

Restatements and Base Year Recalculation

Recalculate base year emissions when:

- Structural changes (acquisition/divestment) exceed threshold (GHG Protocol: typically 5% impact)

- Methodology improvements materially change inventory

- Errors discovered in prior year data

Document restatements in ESG reporting with explanation—stakeholders prefer transparent restatement to silent correction.

Tools and Support for UK Businesses

- DEFRA/DESNZ conversion factors — free annual updates

- GHG Protocol calculation tools — free guidance and spreadsheets

- SECR-compliant templates — Big 4 and specialist consultancies

- Carbon accounting software — scales multi-site data collection

Start with spreadsheets and government factors; invest in software when site count or Scope 3 complexity grows.

Emissions Intensity Metrics

Intensity ratios normalise absolute emissions for business activity:

| Intensity metric | Formula | Common use |

|---|---|---|

| Carbon intensity | tCO₂e / £m revenue | SECR, investor comparison |

| Energy intensity | kWh / unit output | Manufacturing |

| Emissions per FTE | tCO₂e / employee | Services |

Choose intensities relevant to your sector and disclose denominator clearly.

FAQ: Scope 3 Categories at a Glance

| Category | One-line description |

|---|---|

| 1 | Purchased goods and services |

| 2 | Capital goods |

| 3 | Fuel/energy not in Scope 1 or 2 |

| 4 | Upstream transport and distribution |

| 5 | Waste from operations |

| 6 | Business travel |

| 7 | Employee commuting |

| 8 | Upstream leased assets |

| 9 | Downstream transport |

| 10 | Processing of sold products |

| 11 | Use of sold products |

| 12 | End-of-life of sold products |

| 13 | Downstream leased assets |

| 14 | Franchises |

| 15 | Investments |

Screen all 15; deep-dive the material few.

Conclusion

Scope 1, 2 and 3 emissions are the foundation of UK carbon emissions reporting. Master Scope 1 and 2 for SECR compliance, then build Scope 3 capability for TCFD, UK SRS, customer requirements, and credible net zero strategy.

Transparent methodology matters more than false precision—document boundaries, factors, and improvement plans.

Next steps:

- SECR reporting guide — mandatory Scope 1+2

- Sustainability KPIs — track emissions metrics

- What is carbon footprint — organisational footprint context

- Net zero guide — reduction planning

Sources

- GHG Protocol — Corporate Standard and Scope 3 Standard

- UK Government — GHG conversion factors for company reporting

- UK Government — Environmental reporting guidelines including SECR

- IFRS Foundation — IFRS S2 Climate-related Disclosures

This article is for general information only.